Items on this page are from past several months. Some links may no longer be active.

Click on underlined extracts to read full articles.

Haz clic sobre extractos subrayados para leer articulos

completos.

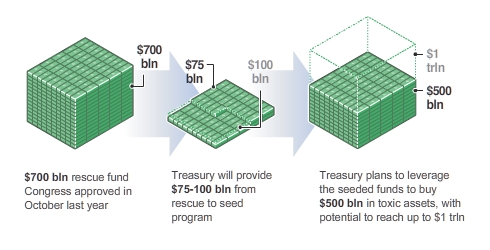

Despite signs that the financial system has stabilized, banks remain threatened by billions of dollars of bad loans on their balance sheets, and more could fail if the economy worsens, a congressional watchdog reports.

In its latest assessment of the $700 billion financial system bailout,

the Congressional Oversight Panel warns that banks still hold many risky loans of uncertain value. If

unemployment rises sharply or the commercial real estate market collapses - as many economists fear - the banking system could again lose its footing, the panel says

in a report to be released Tuesday.

"The financial system (remains) vulnerable to the crisis conditions that (the

bailout) was meant to fix," the panel wrote in a draft copy of Tuesday's report.

The Congressional

Oversight Panel was created as part of the Troubled Asset Relief Program, or TARP. It is designed to provide an additional

layer of oversight, beyond the Special Inspector General for the TARP and regular audits by the Government Accountability

Office.

The report says many of the Obama administration's financial stability

efforts are working - including infusions of new capital for banks, heightened scrutiny of capital ratios, "stress-testing"

of large financial firms. It also pointed to a public-private investment plan designed to buy up bad assets

that has yet to get off the ground.

Bubanks still holding the assets at the heart of the crisis, they

remain vulnerable, the panel says.

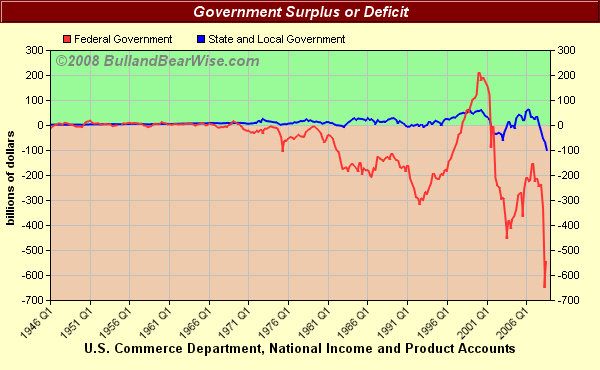

DEFICIT SOARS

The federal budget has gone from surplus to deficit during the past decade.

but uncertainty exists over the speed and duration of the economic recovery, according

to the most recent survey of private economists.

The Blue Chip Economic Indicators survey of private economists released on Monday showed

about 90 percent of the respondents surveyed believe the economic downturn will be declared to have ended this quarter.

This upbeat assessment followed recent government data showing gross domestic product

(GDP) contracted at a shallow 1.0 percent rate in the second quarter after sinking 6.4 percent in the January-March quarter.

Recent data, including housing

and key labor

market indicators, have suggested

a

bottoming in the recession and

the economy

close

to turning the corner

AGGRESSIVE

stimulus spending

by governments helped

the

world avoid a second Great

Depression, but full economic

recovery will take two years

or

more,

Nobel

Prize-winning economist Paul Krugman said...

He added that the worst of the global crisis was over, with economic

and exports growth showing signs of stabilisation.

Still, recovery is likely to be 'disappointing' as government spending

is not sustainable in the long run and the unemployment rate is still lagging behind, he told a two-day World Capital Markets

Symposium on Monday in Kuala Lumpur.

There is not likely to be any 'Phoenix-like' recovery, such as in

the 1997-98 Asian financial crisis when economies expanded dramatically, led by a sharp rebound in exports, he said.

'We have managed to avoid a second Great Depression...but full recovery

is at least two years and probably more,' Mr Krugman said. Asia is likely to see a faster rebound than the United States and

Europe, partly driven by recovery in manufacturing exports, he added.

La disipación de la crisis financiera depende

de las políticas internas, dice Enrique Iglesias

El secretario general Iberoamericano,

Enrique Iglesias, opinó hoy que la disipación de la crisis financiera global dependerá de las políticas internas de las naciones

y exhortó a fortalecer los programas de ayuda social.

For the first time, more than 34 million Americans received

food stamps,

which help poor people buy groceries, government figures said on Thursday, a

sign of the longest and one of the deepest recessions since the Great

Depression

Enrollment surged by 2 percent to reach a record 34.4 million people, or one

in nine Americans, in May, the latest month for which figures are available.

It was the sixth month in a row that enrollment set a record. Every state

recorded a gain in participation from April. Florida had the largest increase at

4.2 percent.

Food stamp enrollment is highest during times of economic stress. The U.S.

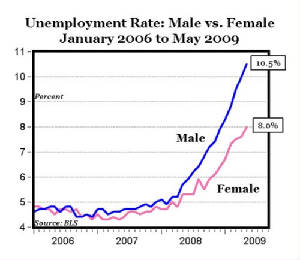

unemployment rate of 9.5 percent is the highest in 26 years.

Average benefit was $133.65 in May per person. The economic stimulus package

enacted earlier this year included a temporary increase in food stamp benefits

of $80 a month for a family of four...CLICK ON STAMPS TO READ MORE

Government Mortgage Program Gets Report Card

The government’s

refinancing and loan modification program is on track to offer assistance to up to three to four million

homeowners over the next three years, according to a Treasury Department report released Tuesday.

The report offered the first glimpse of how the Making Home Affordable Program has made headway in helping troubled

homeowners over the last few months.

More than 235,000 loan modifications and claims are now underway. The Obama

administration has said the program aims to help 500,000 borrowers by Nov.

1.

Examemagazine (one Brazil´s main business publications)

has published a cover story about the recent facts showing that thecrisis in Brazilwas short, and seems to be over.

The

key word here is “facts”. We are not talking about predictions from the same analysts who failed to see

the turmoil faced by the world after mid-2008. Various key indicators confirm that economic activity and job creation

have already undertaken a recovery process. While most of the world´s economies struggle to get out of the hole, Brazilian

economy is again growing.

Some

cases have become symbolic. Let´s take General Motors. While in the United States the car manufacturer is facing

all kinds of problems, and selling part of their Europe assets, in Brazil a R$ 2 billion investment plan is in place to expand

production. The Brazilian auto industry expects to sell 3 million units in 2009, a historic record in a years in which

everyone expected the worst.

A

recessionary scenario seemed realistic for 6 months, with reduction of the GDP, absence of credit, lack of confidence, production

interruption and slowing of sales. This reality is now only seen in the rearview mirror. Brazil is, in fact, experiencing

the next phase: recovery.

Employment

is also entering a considerable recovery process, after predictions pictured a dark. 300,000 new jobs were created on

the first 6 months of 2009, in the economy as a whole. In the end of last year 800,000 jobs were lost in the country, but

in 2009 a positive balance of 600,000 is expected (an exception amongst the world´s 20 largest economies).

It

is interesting to note that a country that has always been hardly hit by the world´s economic turmoils, this time is keeping

its head out of the water based mostly on internal demand. Consumers have not lost their appetite, even with reduction

of credit.

During

the last few weeks, Exame conducted a research with 360 companies in Brazil, which gives us a vision on the current business

and economic climate. Following are some noteworthy facts:

most companies expect considerable growth in Brazil´s GDP in 2009 (54% expect

1% to 3% growth)

48% say the effects of the crisis has diminished in their industry

only 17% do not expect growth in their companies

76% believe growth will be supported mostly or solely by the domestic market

70% are maintaining investments planned before the crisis overall sales are

higher than 1 year ago

cement sales grew 17% since February

vehicles, computers and household appliances are showing strong indications

of growth

consumer credit and real estate also show moderate recovery rates

general industrial production and credit for companies are showing a slower

recovery rate.

96% expect to keep current staffing or hire more people

Cinco consecuencias filosóficas de la crisis

La actual

crisis económica no se limita a una cuestión de estadísticas, ni se reduce al devastador impacto social del desempleo y la

incertidumbre

US State and Local Government Financal

Crisis Now Critical

A recent report by the National Conference of State

Legislatures tallied a total state shortfall of $113.2 billion in FY09 and a gap of $142.6 billion in FY10.Sixteen states, including Georgia,

have unemployment rates over 10%.Georgia

is one of 18 states facing a budget gap of 20% or more of its current budget.

These changes

cannot help but affect education.Utah

has enacted a shorter school year and legislators reduced funding for education by 13% (although part of this cut has been

“backfilled” with stimulus).North

Carolina cut state employee salaries, including teachers, by .5% giving them 10 hours of furlough

“leave.”Also, according to their Legislative Budget Office, teachers

will not receive step increases in FY10.California

has laid off 27,000 teachers.Nevada

cut K-12 teachers salaries by 4%.New

Mexico has cut all state employee pay, including teachers, by 1.5%, but will put the funds back as

an increased contribution to employee pensions.

CALIFORNIA SOLUTION:

LEGALZE AND TAX MARIJUANA

According to one poll, 56 percent of California voters say marijuana should be legalized

and taxed.

As many see it, marijuana is already virtually legal in California where state law allows it for

medical use....Bernard Melekian of the California Police Chiefs Association says "98 percent of the people who are acquiring

marijuana at these dispensaries do not appear to have the conditions for which the law was intended to apply."

Users in Oakland now pay a special city tax on medical marijuana - a first in the state, but maybe

not the last. Marijuana tax promoters say a lot of potential revenue is just going up in smoke.

There is talk in California of what you could call a radical idea for the cash-poor state to raise

money. It's controversial, but proponents say the plan could smoke out more than a billion dollars for the state...

It's

estimated that $14 billion worth of marijuana is sold illegally in the state. Making it legal and taxing it at $50 dollars

an ounce would bring in approximately $1.4 billion a year.

Alabama's debt-ridden Jefferson County laid off about two-thirds

of its 3,600 employees on Monday because of plummeting revenues, a move that will sharply curtail services in areas ranging

from roads to courthouses.

The cuts are just the latest blow to Jefferson, whose population

of 660,000 includesBirmingham,

the state's largest city and its economic powerhouse. They come after the county racked up around $4 billion in debt by using

exotic financial instruments to fund a revamp of its sewer system.

The work-force cuts will hit the roads and transportation, revenue

and security departments, and reductions will also affect the courthouse andinformation technology departmentas

well as laborers paid on an hourly basis, according to a senior county official...

Circuit Judge Joseph L. Boohaker ruled that leaders inJefferson County— now trying to head off a municipalbankruptcy filingof historic

proportions — could go ahead with plans to slash $4.1 million from the budget of Sheriff Mike Hale, who had filed a

lawsuit that temporarily blocked spending cuts for his office.

About 1,000 county workers already are on unpaid leave

because courts threw out a key county tax, and Hale has warned that reductions to his budget would mean fewer patrols by deputies

and decreased courthouse security.

A spokesman for Hale, Randy Christian, said the sheriff

toldGov.

Bob Rileyafter the ruling that state assistance may be needed to performbasic law enforcementtasks once the department's current funding is exhausted in early September.

"We will certainly be looking at calling in the National

Guard," said Christian.

Since

we received fresh data on Friday, it seems like an auspicious time to present a new version of my chart making this point:

The

green bar is the current recession. Most forecasters expect the economy to grow, albeit tepidly, in coming quarters. If they

are right, the estimated peak-to-trough GDP decline in this downturn is 3.9%. ...The chart has three main messages:

The current downturn is the worst since World War II (the green bar is larger than each of the four blue bars).

The current downturn is a far cry from the Great Depression (the green bar is much smaller than the red bar). You would

have to assume enormous further GDP declines to get anywhere near the stunning 26.7% peak-to-trough decline in GDP during

the Depression.

The economy contracted sharply (12.7%, the orange bar) after World War II. That’s why, from a GDP perspective, the

current downturn is the worst since World War II (defined for these purposes as stretching to 1947), not the worst since the

Great Depression.

SEE FULL ARTICLE ON DONALD MARRON'S WEBSITE BY CLICKING ON GLASSES

Warning: Oil supplies are running out fast

Catastrophic shortfalls threaten economic recovery, says world's top energy economist

The world is heading for a catastrophic energy

crunch that could cripple a global economic recovery because most of the major oil fields in the world have passed their peak

production, a leading energy economist has warned.

Higher oil prices brought on by a rapid increase in demand

and a stagnation, or even decline, in supply could blow any recovery off course, said Dr Fatih Birol, the chief economist

at the respected International Energy Agency (IEA) in Paris, which is charged with the task of assessing future energy supplies

by OECD countries.

In an interview with The Independent, Dr Birol said

that the public and many governments appeared to be oblivious to the fact that the oil on which modern civilisation depends

is running out far faster than previously predicted and that global production is likely to peak in about 10 years –

at least a decade earlier than most governments had estimated.

SEE FULL ARTICLE - CLICK ON GLASSES

NATIONAL INFLATION ASSOCIATION

Washington is Clueless About Inflation

It's

unfortunate that nobody in Washington understands what the true definition of inflation is. Inflation is the expansion of

money supply from the printing of money, low reserve requirements, and the Federal Reserve's open market operations. The hyperinflation

in Germany in the 1920's as well as in Zimbabwe today was caused by the government running their printing presses non-stop,

exactly like the U.S. is doing right now.

It just so happens that our massive printing of U.S. dollars has come at

the same time as the biggest bursting of any bubble in world history. Therefore, nobody will see inflation in the form of

rising prices until excess inventories are done being worked off. Eventually there will be too many dollars chasing too few

goods. Remember, none of the stimulus dollars are being spent for the increased production of goods. Manufacturing jobs are

way down and the only area of rising employment is non-productive government jobs.

The U.S. government wants inflation

because inflation benefits debtors and harms creditors, with the U.S. being the largest debtor nation in the world. If the

U.S. wants price inflation and the Federal Reserve takes every step in their power to create it, like they are doing today,

eventually price inflation will arrive but won't be possible to control.

TO READ MORE ON NIA

WEBSITE:

SEE MORE VIDEOS FROM THE NATIONAL INFLATION ASSOCIATION:

The US is on the brink of emerging from its 18-month-long recession according to the International Monetary

Fund, as official figures showed the American economy contracted by just 1pc in the second quarter of the year.

• Focus: Economic and financial

stabilization; developing exit strategies to eventually unwind extraordinary policy support; and dealing with the long-term

legacies of the crisis (weak financial supervision and regulation, massive fiscal imbalances, and damaged household balance

sheets).

• Assessment: Considerable progress has been made toward stabilizing the financial system,

though significant strains remain. The sharp contraction in economic activity is ending, aided by substantial macroeconomic

stimulus. However, the recovery is likely to be gradual, and downside risks prevail.

• Policy advice:

o Stabilization: the priority

is fully healing the financial system. Vigilance is warranted in light of remaining downside risks. Macroeconomic policies

can respond further if risks materialize. o Exiting extraordinary support: key elements include developing strategies

to withdraw public support from the financial system, and to shrink the Fed’s balance sheet, to position it to

pull back on monetary stimulus when a sustainable recovery is underway. Smooth communication will be key to set market

expectations. o Long-term legacies: broad and thorough reforms to financial regulation are needed to deal with

the shortcomings exposed by the crisis. Substantial fiscal adjustment will be needed to stabilize public debt, along

with measures to contain health care costs. Household balancesheet adjustment will likely weigh on growth over the medium

term while narrowing the external imbalance, with global implications.

Last week, President Obama stated his willingness to consider a commission to address our federal fiscal crisis. In an

interview with The Washington Post's Fred Hiatt, the President noted such a commission may be the most realistic

way to begin putting our nation's financial house in order, adding that "everything is going to have to be on the table" for

true fiscal reform.

"I was pleased to read Fred Hiatt's interview of President Obama published in the July 22nd edition of the Washington Post.

During the interview, the President stated his willingness to consider a fiscal commission where 'everything is going to have

to be on the table,' noting it may be the most realistic way to begin putting our nation's financial house in order.

"As I have stated for several years, tough choices must be made in connection with federal budget controls, entitlement

reforms, spending constraints and revenue increases. A properly structured and nonpartisan commission would engage the American

people about the true financial condition of our country and the need for a range of comprehensive reforms. This commission

can lay the groundwork for the ‘grand bargain’ President Obama has said he wants to achieve during his presidency.

"I applaud the President’s recognition that a fiscal commission may be the most productive way to address the serious

financial challenges threatening America's future. Such a commission should include appropriate members of Congress and the

Administration as well as several capable and credible non-governmental experts. After engaging the public and key stakeholders

in new and unprecedented ways, it should make a range of recommendations that would be guaranteed a vote by the Congress.

Ultimately, this extraordinary process can help us avert a much bigger potential economic crisis and ensure that our collective

future is better than our past."

Dave Walker President & CEO Peter G. Peterson Foundation

*Wells Fargo’s 2008 losses include losses from

Wachovia

The Recession

is Over

Now what we need

is a

new kind of

recovery.

The Great

Recession, which rolled over our financial lives like one of P.J. Keating's giant pavers, is most likely over. Home sales,

while still far below the levels of a year ago, have risen for three straight months—a first since 2004. The stock market

has rallied 44 percent since March, thanks to renewed optimism and improving earnings from big companies like Goldman Sachs

and Apple. In June, seven of the 10 indicators in the Conference Board Leading Economic Index pointed upward, including manufacturing

hours worked and unemployment claims. Macroeconomic Advisers, the St. Louis–based consulting firm, says the economy

is expanding at a 2.5 percent annual rate in the current quarter. Economic activity "will increase slightly over the remainder

of 2009," Federal Reserve chairman Ben Bernanke told Congress.

"...we are concerned about the security of the Chinese assets..."

U.S. briefers said the president's team told the Chinese that the United

States was committed to making sure the economic and monetary stimulus being used to fight the recession did not fuel inflation.

U.S. officials told reporters that the U.S. side stressed to the Chinese

that the United States has a plan to bring the deficit down once the economic crisis has been resolved. They said Bernanke

discussed the Fed's exit strategy from the central bank's current period of extraordinary monetary easing, emphasizing that

the Fed was being careful to guard against future inflation.

The Chinese, who have the largest foreign holdings of U.S. Treasury

debt at $801.5 billion, have been expressing worries that soaring deficits could spark inflation or a sudden drop in the value

of the dollar, thus jeopardizing their investments. Chinese officials said those concerns were raised during Monday's talks.

"We sincerely hope the U.S. fiscal deficit will be reduced, year after

year," Assistant Finance Minister Zhu Guangyao told reporters after the Monday talks had ended.

"The Chinese government is a responsible government and first and foremost

our responsibility is the Chinese people, so of course we are concerned about the security of the Chinese assets," Zhu said,

speaking through an interpreter.

The discussions on America's deficits and China's role in financing

them highlighted the growing economic importance of China, now the world's third largest economy...

Bernanke expressed particular opposition

to a proposal in Congress for the Government Accounting Office to be able to "audit" the Fed's interest rate decisions. "I

don't think that's consistent with independence. I don't think the American people want Congress running monetary policy.

That's exactly what (the bill) would do," he said.

"...once the recovery began – in different calendar years in different countries – the

average rate of growth was strong. GDP growth in the first year after the Great Depression averaged 4.7 per cent, followed

by 4.6 per cent in the second and third years...

The world economy is in its worst recession since the early ’80s.

During the second half of 2008 world credit markets froze and international

trade suffered a sudden 20% decline. The slump in world trade resulted in a sharp fall in exports in the major and emerging

markets, confirming that the world economy is more interlinked than ever through trade and capital flows.

In recent months credit markets have started to thaw. As credit flows normalised,

so bank and corporate bond spreads narrowed sharply from historic highs. Many economic indicators are starting to show signs

of recovery.

Government and central bank policies restored some investor confidence in

financial markets and equity prices recovered ground as fears of a ’30s-style depression receded.

Although government and central bank policies appear to be gaining traction,

we believe there are longer-term costs to these policies. Extremely low interest rates are not sustainable over the long term

and as economic activity revives, interest rates need to rise.

IFAC has launched a resource center

to help professional accountants address issues related to the global financial crisis. The center (http://www.ifac.org/financial-crisis/) serves as an international clearinghouse of programs,

articles, speeches, and other initiatives undertaken by IFAC, its independent standard-setting boards, members and associates,

as well as other organizations that are relevant to professional accountants.

To assist professional accountants in addressing

issues related to the global financial crisis, IFAC and the International Auditing and Assurance Standards Board (IAASB) have

focused on three activities:

+ To increase awareness among preparers and

auditors of existing and newly developed guidance that can assist them in reporting on financial instruments;

+ To encourage further convergence in reporting

standards on financial instruments, while at the same time strongly supporting (the continuation of) fair value accounting

since reducing transparency is not in the interests of investors; and

+ To participate in and promote discussions

of best practice with respect to the audits of financial institutions and other organizations that are affected by the current

crisis.

View President Obama's July 22 Health Reform Press Conference (approx. 1 hour)

The economic indicators we follow to track real economic activity

are all signaling a slowdown of massive proportions. You wouldn’t know it reading the mainstream papers of course

– they all focus on the relative decline in the slowdown’s intensity. Reading about the slowdown ‘slowing

down’ is not the same as growth however, and does not warrant excitement in our opinion.

We

find the similarity between the 2008 economic collapse and the 1929 economic collapse disturbing. Don’t get sucked

in… the real economy is still struggling and the market has yet to reflect this. In 1932, the

Dow

Jones Industrial Average bottomed 90% below the September 1929 peak. The S&P 500 Index peaked in October 2007 at

1,576, and from our brief analysis above we can easily calculate a drop in the S&P 500 of as much as 88% from that

peak using our ‘double trouble’ scenario. At the very least, under all of our scenarios it appears that the

S&P 500 Index will test the March 2009 low of 666. Judging by the continued declines we are seeing in the real economy,

we expect that test to happen sooner rather than later.

In our view, the only thing propping

this market up is investor sentiment. Earnings have not improved.

US

industry used only 68.3% of available capacity in May 2009, according to a monthly report from the Federal Reserve.1

That represents almost one third of all US industrial capacity sitting idle. Prior to the current recession, the lowest

rate recorded since the Fed started this series of records in 1967 was 70.9% in December 1982.

The

US government has spent $2.67 trillion thus far in fiscal 2009, but has only collected $1.59 trillion.

The

US government collected $685.5 billion in individual income taxes so far this year, a 22% drop from the $877.8 billion

the government took in during the first nine months of 2008.

US corporate income taxes plunged 57%

to $101.9 billion in 2009, down from $236.5 billion in the first nine months of fiscal year 2008.

4

million Americans have been looking for work for more than 26 weeks, representing

29% of the unemployed

– the most since records began in 1948.

During the last 30 years, Americans who lost their jobs

took an average 15.8 weeks to find new positions. In June 2009, the average duration of unemployment was 24.5 weeks,

the longest since records began in 1948.

The number of people collecting unemployment benefits

reached a record 6.88 million in the week ended June 27, 2009.

Approximately six people are seeking

work for every job opening, the most since the government began keeping such records in 2000. A year ago, the ratio was

a little more than two-to-one...Sprott

Asset Management

Are

We in the Early Stages of a Economic Depression? A Comment on the above analysis

I do not disagree...The risks in our economy remain exceptionally

high. The stock market is in the process of defining winners and losers but overall is being supported by massive liquidity

injected into the overall economy by Uncle Sam (Fed and Treasury).

What

may cause the next leg down in the economy? Commercial real estate defaults which will impact a large number of banks (community,

regional, and money center) and insurance companies.

Recession?

Depression? Let’s just say by either definition, we have a long way to go.

For a glimpse of what awaits

Britain, Europe, and America as budget deficits spiral to war-time levels, look at what is happening to the Irish welfare

state.

Events have already forced Premier Brian Cowen to carry out the harshest assault yet

seen on the public services of a modern Western state. He has passed two emergency budgets to stop the deficit soaring to

15pc of GDP. They have not been enough...

The Fed's doctrine – New Keynesian Synthesis – has

let it down time and again in this long saga, and there is scant evidence that Fed officials recognise the fact. As for the

European Central Bank, it has let private loan growth contract this summer.

The imperative for the debt-bloated West is to cut spending systematically

for year after year, off-setting the deflationary effect with monetary stimulus. This is the only mix that can save us.

Bernanke

afirmó que el plan anticrisis no provocará inflación en EE.UU.

El presidente de la Fed aseguró que la entidad posee "numerosas herramientas eficaces para ajustar la

política monetaria" cuando la economía retome la senda del crecimiento; advirtió que se mantendrá el desempleo

(NOTE: By comparison the estimated population

offishin

the oceans is 3,500,000,000,000

or 3.5 trillion...

the estimated number of humans on Earth is

6,760,000,000 or 6.76 billion...

and the estimated number of ants is

200,000,000,000,000 or 200 trillion

thus $23.7 Trillion

=

$3,506 per human being

or $ 6.77 per

fish

or 12 ¢ per ant)

The total price tag for federal support stemming from

the financial crisis could reach $23.7 trillion in the long run, the government's top bailout watchdog says in a new report

to Congress.

Neil Barofsky, the inspector general for the Troubled

Asset Relief Program, plans to deliver his report Tuesday to the House Oversight and Government Reform Committee.

The $23.7 trillion figure is admittedly a high-ball

number and reflects the total potential gross exposure, but Barofsky in his prepared testimony notes that the TARP -- which

started as a $700 billion bailout -- has expanded well beyond that.

"TARP has evolved into a program of unprecedented scope,

scale and complexity. Moreover, TARP does not function in a vacuum but is rather part of the broader government efforts to

stabilize the financial system," the report says.

"The total potential federal government support could

reach up to $23.7 trillion," the report estimates, factoring in commitments from "dozens of programs" implemented throughout

the federal government since 2007

"A trillion here, a trillion there will get things

stabilized"

Gary Schilling

I think that what the government has done so far, despite the trillions of dollars,

is questionable. People are miserable. They are saving all their cash, their social-security checks, and many people are still

in big trouble. Modifications of troubled mortgages are proceeding slowly, and those that are modified are proving to be serial

defaulters. More than 50 percent are behind in payments.

What people need is a consumer subsidy to help them handle

their mortgages. The government gave trillions of dollars for bailout programs -- now it should give another trillion to consumers.

A trillion here, a trillion there will get things stabilized...

Of $3.1 trillion in total commercial real estate debt, banks and thrifts hold $1.7 trillion

in mortgages. Another $700 billion is securitized, and the delinquency rate more than tripled in six months, to 2.7 percent

in May, the highest in a decade. Default rates are expected to hit 30 percent or more, and loss rates could reach 13 percent...

The estimates are that $155 billion in securitizations are coming due by 2012, and two-thirds

won't qualify for refinancing as prices drop 35 percent to 45 percent from their 2007 peaks. Meanwhile, $525 billion of commercial mortgages

held by banks and thrifts will come due by 2012. About 50 percent won't qualify for refinancing because they exceed 90 percent

of the underlying property value. Lenders prefer loans of no more than 65 percent...

I have been saying it will go for a second stimulus package. The first one was for education,

health and the environment, and was intended to put people to work. There is a lot of resistance to another package, though,

and further increases to the deficit. Our estimate is that $200 billion went to stimulus for infrastructure, unemployment

and tax cuts, and the rest was for social agenda: education, health and environment...

It will extend into early 2010. Only by then is enough fiscal stimulus likely to be pumped out to stabilize

consumer retrenchment. By then, enough excess house inventories may be absorbed to moderate the downward pressure on prices.

By then, most of the global financial woes should be at least stabilized. Nevertheless, a weak recovery is likely to follow,

one so tepid and with such high unemployment that you may not know it has arrived.

Is securitization like a financial terrorist attack?

A recent editorial in the Wall Street Journal makes it clear that securitization -- the packaging of thousands of loans

into securities -- has all the features of a successful terrorist attack. How so? It entered the financial system without

attracting any negative notice at all, found its way into the heart of the global financial markets and, once ensconced there,

proceeded to destroy the system (and is continuing to do so now).

In fact, securitization is proving to be more costly from a financial standpoint than everything that al Qaeda has cooked

up against us. So far, the financial rescue has cost $12.8 trillion and that figure could reach as high as $23.7 trillion.

The wars in Iraq and Afghanistan cost only $3 trillion at most. (To be fair, though, securitization has taken a far smaller

human toll than al Qaeda.)

Why do I blame securitization for our current financial calamity? Remember toxic waste? That's the $13 trillion worth

of residential mortgage-backed securities (MBS) -- bundles of mortgages sliced by level of risk -- and collateralized debt

obligations (CDOs) -- mixed bundles of commercial mortgages, auto loans, student loans, credit card receivables, small business

loans, and corporate loans sorted by risk level -- residing on the books of financial institutions around the globe.

Securitization is not the sole problem -- it is the fact that some financial institutions (FIs) leveraged up their balance

sheets 50:1 to buy the toxic waste. And they bought it because they believed that in a low-interest-rate environment, they

thought they were getting a safe, higher-yielding investment...

Under current law, the federal budget is on an unsustainable

path, because federal debt will continue to grow much faster than the economy over the long run. Although great uncertainty

surrounds long-term fiscal projections, rising costs for health care and the aging of the population will cause federal spending

to increase rapidly under any plausible scenario for current law. Unless revenues increase just as rapidly, the rise in spending

will produce growing budget deficits. Large budget deficits would reduce national saving, leading to more borrowing from abroad

and less domestic investment, which in turn would depress economic growth in the United States. Over time, accumulating

debt would cause substantial harm to the economy. The following chart shows our projection of federal debt

relative to GDP under the two scenarios we modeled.

Federal Debt Held by the Public Under CBO’s Long-Term Budget Scenarios

(Percentage of GDP)

Keeping deficits and debt from reaching these levels would

require increasing revenues significantly as a share of GDP, decreasing projected spending sharply, or some combination of

the two.

Measured relative to GDP, almost all of the projected growth

in federal spending other than interest payments on the debt stems from the three largest entitlement programs—Medicare,

Medicaid, and Social Security. For decades, spending on Medicare and Medicaid has been growing faster than the economy. CBO

projects that if current laws do not change, federal spending on Medicare and Medicaid combined will grow from roughly 5 percent

of GDP today to almost 10 percent by 2035. By 2080, the government would be spending almost as much, as a share of the economy,

on just its two major health care programs as it has spent on all of its programs and services in recent years.

In CBO’s estimates, the increase in spending for Medicare

and Medicaid will account for 80 percent of spending increases for the three entitlement programs between now and 2035 and

90 percent of spending growth between now and 2080. Thus, reducing overall government spending relative to what would occur

under current fiscal policy would require fundamental changes in the trajectory of federal health spending. Slowing the growth

rate of outlays for Medicare and Medicaid is the central long-term challenge for fiscal policy.

Under current law, spending on Social Security is also projected

to rise over time as a share of GDP, but much less sharply. CBO projects that Social Security spending will increase from

less than 5 percent of GDP today to about 6 percent in 2035 and then roughly stabilize at that level. Meanwhile, as depicted

below, government spending on all activities other than Medicare, Medicaid, Social Security, and interest on federal debt—a

broad category that includes national defense and a wide variety of domestic programs—is projected to decline or stay

roughly stable as a share of GDP in future decades.

Spending Other Than That for Medicare, Medicaid, Social Security,

and Net Interest, 1962 to 2080 (Percentage of GDP)

Federal spending on Medicare, Medicaid, and Social Security

will grow relative to the economy both because health care spending per beneficiary is projected to increase and because the

population is aging. As shown in the figure below, between now and 2035, aging is projected to make the larger contribution

to the growth of spending for those three programs as a share of GDP. After 2035, continued increases in health care spending

per beneficiary are projected to dominate the growth in spending for the three programs.

Factors Explaining Future Federal Spending on Medicare, Medicaid,

and Social Security (Percentage of GDP)

The current recession and policy responses have little effect

on long-term projections of noninterest spending and revenues. But CBO estimates that in fiscal years 2009 and 2010, the federal

government will record its largest budget deficits as a share of GDP since shortly after World War II. As a result of those

deficits, federal debt held by the public will soar from 41 percent of GDP at the end of fiscal year 2008 to 60 percent at

the end of fiscal year 2010. This higher debt results in permanently higher spending to pay interest on that debt. Federal

interest payments already amount to more than 1 percent of GDP; unless current law changes, that share would rise to 2.5 percent

by 2020.

This entry was posted on Thursday, July

16th, 2009

VP Joe Biden: ‘We Have to Go Spend Money to Keep From Going Bankrupt’

Vice President Joe Biden (Photo

by Penny Starr/CNSNews.com)

Vice President Joe Biden

told people attending an AARP town hall meeting that unless the Democrat-supported health care plan becomes law the nation

will go bankrupt and that the only way to avoid that fate is for the government to spend more money...the president

knows, and I know, that the status quo is simply not acceptable,” Biden said...“It’s totally unacceptable.

And it’s completely unsustainable. Even if we wanted to keep it the way we have it now. It can’t do it financially.”

“We’re

going to go bankrupt as a nation,” Biden said.

“Now, people when I say that look at me and say,

‘What are you talking about, Joe? You’re telling me we have to go spend money to keep from going bankrupt?’”

Biden said. “The answer is yes, that's what I’m telling you.”

IT HAS ONLY BEEN IN THE LAST 8 YEARS

THAT THE % OF INCOME SPENT BY AMERICANS HAS BEEN IN SINGLE DIGITS...before the year 2000 it was over 10% and until the 1950's

it was over 20%.

Estudio económico de América Latina

y el Caribe 2008-2009

Comisión Económica para América

Latina y el Caribe (CEPAL)

RESUMEN

La publicación del sexagésimo primer Estudio económico de América Latina y el Caribe, correspondiente

al bienio 2008-2009, tiene lugar en un momento crítico del desarrollo económico de América Latina y el Caribe. Se interrumpió

una fase de crecimiento de duración y características inéditas en la historia reciente y la región sufre una contracción de

su producto, con efectos negativos en el bienestar de la población que inevitablemente se reflejarán en retrocesos de las

variables sociales. Dos características diferencian la situación actual de los muchos episodios de crisis que afectaron a

la región en las décadas pasadas. En primer lugar, la crisis no se originó en la región ni tampoco en otra economía emergente,

sino en la economía más grande del mundo, por lo que tuvo efectos a nivel global, con significativas diferencias entre países

y regiones. En segundo lugar, si bien con excepciones significativas, al disminuir sus deudas e incrementar sus reservas durante

la fase expansiva de los años pasados, la región en su conjunto está mejor preparada para enfrentar esta crisis que en episodios

previos y que otras regiones. Estas características, por su parte, tienen dos consecuencias: la tasa de contracción proyectada

para el año en curso es relativamente moderada —si bien nuevamente con marcadas diferencias entre los países de la región—

y la recuperación depende en gran parte de la reactivación de la economía mundial en su conjunto.

En la primera parte de este Estudio económico se analizan los canales a través de los cuales

la crisis está afectando a las economías de la región y su efecto en variables como el crecimiento económico, el empleo y

los indicadores del sector externo. También se presentan las fortalezas y debilidades para enfrentar las consecuencias de

la crisis mundial y las políticas económicas aplicadas en este contexto. El análisis abarca la evolución de la economía regional

en 2008 y el primer semestre de 2009 y concluye con un examen de las perspectivas de la región en el segundo semestre del

año, todo ello respaldado con un amplio anexo estadístico.

Las características de la recuperación dependen en gran medida de la evolución de la economía

mundial, pero también de la manera en que los países se preparan para los desafíos del futuro. A este respecto, es importante

el manejo macroeconómico de la crisis, pero también, como la CEPAL ha enfatizado en repetidas ocasiones, la construcción de

los fundamentos para un crecimiento sostenido, basado en una creciente competitividad sistémica, una mayor cohesión social

y una estructura productiva y de consumo ambientalmente sostenible. Por lo tanto, una tarea clave de los países de la región

es el desarrollo de instituciones acordes con estos objetivos. En este Estudio económico se analiza el caso de la institucionalidad

laboral, que en el pasado reciente ha sido objeto de confrontaciones polarizadas y debates sumamente controvertidos. No obstante,

actualmente se han abierto espacios para un debate más equilibrado que tome en cuenta que esta institucionalidad debe cumplir

con varios objetivos, lo que no permite la imposición de visiones particulares.

En el primer capítulo de la segunda parte se revisa el desarrollo histórico de la institucionalidad

laboral de la región, la gran variedad existente al respecto entre los países y el papel de los principales componentes de

esta institucionalidad. En el segundo capítulo, se presentan los cambios recientes en algunas instituciones específicas, el

salario mínimo, los sindicatos y la negociación colectiva, así como los instrumentos de protección al desempleo, y se analizan

sus efectos sobre el funcionamiento del mercado de trabajo y las opciones para su perfeccionamiento. En el tercer capítulo,

se examinan las políticas activas del mercado de trabajo, específicamente la capacitación y formación profesional, los servicios

públicos de empleo, la generación directa e indirecta de empleo y el fomento del trabajo independiente. En el cuarto capítulo,

se discuten alternativas de política para promover la inserción laboral productiva de los jóvenes y las mujeres, quienes con

frecuencia son marginados y discriminados en el mercado laboral. El quinto capítulo resume las conclusiones sobre los desafíos

de la institucionalidad laboral y los mecanismos para avanzar en el cumplimiento de sus objetivos.

Por último, se analiza la coyuntura de los países de América Latina y el Caribe en 2008 y el

primer semestre de 2009. A la información de las notas de cada país se suman los datos del anexo estadístico en el que se

muestra la evolución de los principales indicadores económicos. Estas notas, al igual que el anexo estadístico específico

para cada país, se publican en el CD-ROM que acompaña la versión impresa, así como también en la página web de la CEPAL (www.cepal.org). En los cuadros del anexo estadístico se puede visualizar rápidamente la información de los

últimos años y crear cuadros en hojas electrónicas. En el disco se encuentran también las versiones electrónicas de la primera

y la segunda parte.

La información estadística de la presente publicación ha sido actualizada al 30 de junio de

2009. Haz clic en su pais para el contenido...

From FORBES: The U.S. economic outlook

remains very weak.

The United States is in the twentieth month of a recession that has been by

far the longest and most severe of the postwar period. While comparisons with the Great Depression are frequent and appropriate

(especially if we look at the pace of contraction in industrial production), the aggressiveness of policy measures has significantly

reduced the probability of a near-depression.

"Banking Establishments Are More Dangerous Than Standing Armies." Thomas Jefferson

(1743-1826), 3rd US President

"...

a serious depression seems improbable; [we expect] recovery of business next spring, with further improvement in the fall."

Harvard Economic Society (HES), November 10, 1929

"While

the crash only took place six months ago, I am convinced we have now passed through the worst -- and with continued unity

of effort we shall rapidly recover. There has been no significant bank or industrial failure. That danger, too, is safely

behind us." President Herbert Hoover, May 1, 1930

"Under

a paper money system, a determined government can always generate higher spending and hence positive inflation." Fed Chairman

Ben Bernanke, in 2002

Many

observers think that “prosperity is around the corner” and that this recession, like others since World War II,

will end as soon as the stock market, as a leading indicator, recovers and people start spending again. This is a myopic view

of the current economic big picture.

In fact, since the peak of the housing bubble (in the U.S.) in 2005, the onslaught of the subprime financial

crisis in August 2007 and the beginning of the recession in December 2007, the U. S. economy, and to a certain extent, the

world economy, have entered a period of protracted adjustments. For sure, there will be some quarters of positive economic

growth ahead and the recession may be declared officially over in the coming months, but the radical economic reorganization

that is taking place will go on for years to come...........................................................................................

For

now, a quick resurgence of inflation is only a remote possibility. This is nevertheless a possibility, considering that central

banks have a tendency to overdo the printing of fiat money. In fact, if governements attempt to print their way out of the

coming structural demographic problem, they will end up generating an hyperstagflation. In a nutshell, this is what the huge

international dollar-denominated bond market sees and fears, at a time when it has to absorb a huge supply of new bond issues.

In reality, the bond market will always win against any central bank, any time. The solvency woes and the likely default of

the state of California on its outstanding debt will only add to the anxiety.

A

few weeks ago, I warned against the risk of future long term interest rates hikes and future U.S. dollar depreciation following

the decisions by the U.S. Treasury and by the Fed to flood the markets with trillions of dollars of new Treasury bond issues

and with newly printed money. The undertow is coming even faster than I thought. Only when the markets expect relative economic

stagnation and a lasting deflationary environment will long term interest rates taper off.

Brace yourself and hold on to your britches. There is a rough economic decade ahead.

In a year of eye-popping numbers, add one more: The government's annual

budget deficit has topped $1 trillion.

And

with three months left in the budget year, it will actually get even worse. The administration is projecting that the deficit

will hit $1.84 trillion for the current budget year, four times the size of last year's deficit. Last year's number was the

all-time leader at the time, at $454.8 billion — a figure that now seems rather puny in comparison.

Here

are some questions and answers about what happened to the federal budget, which began the new century with the longest string

of surpluses in seven decades.

Q:

Just how did we go from a string of four consecutive surpluses from 1998 through 2001 to the fix we are in now?

A:

The surpluses at the end of the last decade reflected a boom-time economy, which was enjoying the longest uninterrupted expansion

in U.S. history.

When

the last recession began in 2001, that cut into revenues. Then the government's budget picture darkened even further after

the 2001 terrorist attacks as government spending was increased to pay for wars in Afghanistan and Iraq.

“I don’t think the worst

is over ... It’s very likely that more jobs will be lost. It would not be surprising if GDP has not yet reached its

low. What does appear to be true is that the sense of panic in the markets and freefall in the economy has subsided and one

does not have the sense of a situation as out of control as a few months ago.”

As the panic

has subsided, the trendy new economic issue has become “exit strategy” – as in, when and how do governments

shift from costly and aggressive intervention to levels of spending and taxation that are sustainable over the long term?

Summers rejects the premise of the

question. “I actually think that the right measures for doing the right things about the long-run deficit will also

increase confidence, hold down long-term interest rates and capital costs, make mortgages cheaper, make mortgage rates lower

and so will contribute directly to recovery. So I don’t buy the notion that there is some conflict between the budget

imperative for growth and some other budget imperatives.”

Larry Summers, director of the US president’s

National Economic Council in interview with Financial Times

DE LA IZQUIERDA...si o no esta de acuerdo, deberia leer esto

Crisis del Capitalismo, el ALBA TCP y la unidad de la Clase

Trabajadora

Consideraciones sobre la Crisis del Capitalismo

Vivimos momentos históricos estelares, la crisis mundial del capitalismo apenas ha mostrado

sus primeros síntomas en las economías de los centros del imperialismo. La crisis financiera cada vez más es acompañada por

una crisis del crédito que repercutirá sin lugar a dudas a las esferas productivas del capitalismo. En este sentido, los monopolios

industriales han sido golpeados de forma contundente y unos que incluso constituían modelos del capitalismo monopolista transnacionalizado

han caído estrepitosamente, General Motors es el caso más dramático, porque era considerada la joya de la industria automovilística

norteamericana.

Está claro para muchos que la crisis actual del capitalismo no tiene precedentes, ya que

afecta de forma simultánea diversos aspectos del sistema; a la profunda crisis financiera, se le suman crisis energéticas,

alimentarias y la más grave, una crisis ambiental creciente. Eso sin contar el conjunto de crisis y contradicciones políticas,

sociales, humanitarias que afectan a diversos pueblos: agresiones imperialistas, los genocidios, las guerras civiles, el narcotráfico,

el comercio sexual, son sólo algunos de los fenómenos degradantes inherentes al capitalismo realmente existente, el Comandante

Hugo Chávez ha hablado en este sentido de una profunda crisis moral...

...el ALBA TCP

tiene por objetivo la transformación de las sociedades latinoamericanas, haciéndolas más justas, cultas, participativas y

solidarias y por tanto está concebida como un proceso integral destinado a asegurar la eliminación de las desigualdades sociales

y fomentar la calidad de vida y una participación efectiva de los pueblos en la conformación de su propio destino.

Russian President Dmitry Medvedev holds up an 'worldwide coin' as he discusses a

possible

global currency

Even if Russia's call for a

global currency failed to gain much traction at a G8 summit, President Dmitry Medvedev took home a coin meant to symbolize that the dream may one day come true.

The Russian leader proudly displayed the coin, which bears the English words "United

Future World Currency", to journalists after the summit wrapped up in the quake-hit Italian town of L'Aquila.

Medvedev said that although the coin, which resembled a euro and featured the image

of five leaves, was just a gift given to leaders it showed that people were beginning to think seriously

about a new global currency.

____________________

Role of information

technology in economic

recovery

***

about half of today's Fortune 500 companies were launched during a recession...

***

companies can help themselves and the country out of its funk through research, development and innovation...

***

"There is an unnatural opportunity and responsibility to help drive the productivity and innovation that can let the economy

come back and grow again”...

***

“It is a tough time, but it is a time for those of us in the technology industry to say, ‘Hey, it's our

time. It's our time to do something great.'”

The world financial crisis offers organized crime

a unique opportunity to return to the global banking systems from which it had been barred by sanctions imposed after the

Sept. 11, 2001 terror attacks, the U.N.'s top anti-crime official said

Pope Benedict issued anambitious call to reformthe way the world works on Tuesday shortly before

its most powerful leaders meet at theG8 summit in Italy. His latest encyclical, entitled “Charity in Truth,” presents along list of stepshe thinks are needed to overcome the financial

crisis and shift economic activity from the profit motive to a goal of solidarity of all people.

Following are some of his proposals. The italics are from theoriginal text.

“There is urgent need of a true world political authority. ..to

manage the global economy; to revive economies hit by the crisis; to avoid any deterioration of the present crisis and the

greater imbalances that would result; to bring about integral and timely disarmament, food security and peace; to guarantee

the protection of the environment and to regulate migration… such an authority would need to be universally recognized

and to be vested with the effective power to ensure security for all, regard for justice, and respect for rights.”

The economy needs ethics in order to function correctly-

not any ethics whatsoever, but an ethics which is people-centred…”

“Financiers must rediscover the genuinely ethical foundation of their activity, so as

not to abuse the sophisticated instruments which can serve to betray the interests of savers. Right intention, transparency,

and the search for positive results are mutually compatible and must never be detached from one another.”

“Without doubt, one of the greatest risks for businesses is that they are almost exclusively

answerable to their investors, thereby limiting their social value… there is nevertheless a growing conviction thatbusiness management cannot concern itself only with the interests of the proprietors,

but must also assume responsibility for all the other stakeholders who contribute to the life of the business: the workers,

the clients, the suppliers of various elements of production, the community of reference… What should be avoided is

a speculativeuse of financial resourcesthat

yields to the temptation of seeking only short-term profit, without regard for the long-term sustainability of the enterprise,

its benefit to the real economy and attention to the advancement, in suitable and appropriate ways, of further economic initiatives

in countries in need of development.”

“One possible approach to development aid would be to apply effectively what is known

as fiscal subsidiarity, allowing citizens to decide how to allocate a portion of the taxes they pay to the State.”

Sigue la síntesis facilitada por la Oficina de Prensa

de la Santa Sede de la nueva encíclica de Benedicto XVI, "Caritas in veritate": La Caridad en la verdad, sobre el desarrollo

humano integral en la caridad y en la verdad .

La Encíclica, publicada hoy, consta de una introducción,

seis capítulos y una conclusión y está fechada el 29 de junio de 2009, solemnidad de San Pedro y San Pablo.

"En la Introducción -explica la síntesis- el Papa recuerda

que la caridad es "la vía maestra de la doctrina social de la Iglesia". Por otra parte, dado el "riesgo de ser mal entendida

o excluida de la ética vivida" advierte de que "un cristianismo de caridad sin verdad se puede confundir fácilmente con una

reserva de buenos sentimientos, provechosos para la convivencia social, pero marginales".

"El desarrollo (...) necesita esta verdad", escribe

Benedicto XVI y analiza "dos criterios orientadores de la acción moral: la justicia y el bien común. (...) Todo cristiano

está llamado a esta caridad, según su vocación y sus posibilidades de incidir en la polis. Ésta es la vía institucional del

vivir social".

El primer capítulo está dedicado al "Mensaje de la

"Populorum progressio" de Pablo VI que "reafirmó la importancia imprescindible del Evangelio para la construcción de la sociedad

según libertad y justicia". "La fe cristiana -escribe Benedicto XVI- se ocupa del desarrollo no apoyándose en privilegios

o posiciones de poder (...) sino solo en Cristo". El pontífice evidencia que "las causas del subdesarrollo no son principalmente

de orden material". Están ante todo en la voluntad, el pensamiento y todavía más "en la falta de fraternidad entre los hombres

y los pueblos".

"El desarrollo humano en nuestro tiempo" es el tema

del segundo capítulo. "El objetivo exclusivo del beneficio, cuando es obtenido mal y sin el bien común como fin último -reitera

el Papa- corre el riesgo de destruir riqueza y crear pobreza" Y enumera algunas distorsiones del desarrollo: una actividad

financiera "en buena parte especulativa", los flujos migratorios "frecuentemente provocados y después no gestionados adecuadamente

o la explotación sin reglas de los recursos de la tierra". Frente a esos problemas ligados entre sí, el Papa invoca "una nueva

síntesis humanista", constatando después que "el cuadro del desarrollo se despliega en múltiples ámbitos: (...) crece la riqueza

mundial en términos absolutos, pero aumentan también las desigualdades (...) y nacen nuevas pobrezas".

"En el plano cultural -prosigue- (...) las posibilidades

de interacción" han dado lugar a "nuevas perspectivas de diálogo", (...) pero hay un doble riesgo". En primer lugar "un eclecticismo

cultural" donde las culturas se consideran "sustancialmente equivalentes". El peligro opuesto es el de "rebajar la cultura

y homologar los (...) estilos de vida". Benedicto XVI recuerda "el escándalo del hambre" y auspicia "una ecuánime reforma

agraria en los países en desarrollo".

Asimismo, el pontífice evidencia que el respeto por

la vida "en modo alguno puede separarse de las cuestiones relacionadas con el desarrollo de los pueblos" y afirma que "cuando

una sociedad se encamina hacia la negación y la supresión de la vida acaba por no encontrar la motivación y la energía necesarias

para esforzarse en el servicio del verdadero bien del hombre".

Otro aspecto ligado al desarrollo es el "derecho a

la libertad religiosa. La violencia - escribe el Papa-, frena el desarrollo auténtico" y esto "ocurre especialmente con el

terrorismo de inspiración fundamentalista".

"Fraternidad, desarrollo económico y sociedad civil"

es el tema del tercer capítulo, que se abre con un elogio de la experiencia del don, no reconocida a menudo, "debido a una

visión de la existencia que antepone a todo la productividad y la utilidad. (...) El desarrollo, (...) si quiere ser auténticamente

humano, necesita en cambio dar espacio al principio de gratuidad", y por cuanto se refiere al mercado la lógica mercantil,

ésta debe estar "ordenada a la consecución del bien común, que es responsabilidad sobre todo de la comunidad política".

Retomando la encíclica "Centesimus annus" indica "la

necesidad de un sistema basado en tres instancias: el mercado, el Estado y la sociedad civil" y espera en "una civilización

de la economía". Hacen falta "formas de economía solidaria" y "tanto el mercado como la política tienen necesidad de personas

abiertas al don recíproco".

El capítulo se cierra con una nueva valoración del

fenómeno de la globalización, que no se debe entender solo como "un proceso socio-económico". (...) La globalización necesita

"una orientación cultural personalista y comunitaria abierta a la trascendencia (...) y capaz de corregir sus disfunciones".

En el cuarto capítulo, la Encíclica trata el tema del

"Desarrollo de los pueblos, derechos y deberes, ambiente". "Gobierno y organismos internacionales -se lee- no pueden olvidar

"la objetividad y la indisponibilidad" de los derechos. A este respecto, se detiene en las "problemáticas relacionadas con

el crecimiento demográfico".

Reafirma que la sexualidad no se puede "reducir a un

mero hecho hedonístico y lúdico". Los Estados, escribe, "están llamados a realizar políticas que promuevan la centralidad

de la familia".

"La economía -afirma una vez más- tiene necesidad de

la ética para su correcto funcionamiento; no de cualquier ética sino de una ética amiga de la persona". La misma centralidad

de la persona, escribe, debe ser el principio guía "en las intervenciones para el desarrollo" de la cooperación internacional.

(...) Los organismos internacionales -exhorta el Papa- deberían interrogarse sobre la real eficacia de sus aparatos burocráticos",

"con frecuencia muy costosos".

El Santo Padre se refiere más adelante a las problemáticas

energéticas. "El acaparamiento de los recursos" por parte de Estados y grupos de poder, denuncia, constituyen "un grave impedimento

para el desarrollo de los países pobres". (...) "Las sociedades tecnológicamente avanzadas -añade- pueden y deben disminuir

la propia necesidad energética", mientras debe "avanzar la investigación sobre energías alternativas".

"La colaboración de la familia humana" es el corazón

del quinto capítulo, en el que Benedicto XVI pone de relieve que "el desarrollo de los pueblos depende sobre todo del reconocimiento

de ser una sola familia". De ahí que, se lee, la religión cristiana puede contribuir al desarrollo "solo si Dios encuentra

un puesto también en la esfera pública".

El Papa hace referencia al principio de subsidiaridad,

que ofrece una ayuda a la persona "a través de la autonomía de los cuerpos intermedios". La subsidiariedad, explica, "es el

antídoto más eficaz contra toda forma de asistencialismo paternalista" y es más adecuada para humanizar la globalización".

Asimismo, Benedicto XVI exhorta a los Estados ricos

a "destinar mayores cuotas" del Producto Interno Bruto para el desarrollo, respetando los compromisos adquiridos. Y augura

un mayor acceso a la educación y, aún más, a la "formación completa de la persona" afirmando que, cediendo al relativismo,

se convierte en más pobre. Un ejemplo, escribe, es el del fenómeno perverso del turismo sexual. "Es doloroso constatar -observa-

que se desarrolla con frecuencia con el aval de los gobiernos locales".

El Papa afronta a continuación al fenómeno "histórico"

de las migraciones. "Todo emigrante, afirma, "es una persona humana" que "posee derechos que deben ser respetados por todos

y en toda situación".

El último párrafo del capítulo lo dedica el Pontífice

"a la urgencia de la reforma" de la ONU y "de la arquitectura económica y financiera internacional". Urge "la presencia de

una verdadera Autoridad política mundial" (...) que goce de "poder efectivo".

El sexto y último capítulo está centrado en el tema

del "Desarrollo de los pueblos y la técnica". El Papa pone en guardia ante la "pretensión prometeica" según la cual "la humanidad

cree poderse recrear valiéndose de los 'prodigios' de la tecnología". La técnica, subraya, no puede tener una "libertad absoluta".

El campo primario "de la lucha cultural entre el absolutismo

de la tecnicidad y la responsabilidad moral del hombre es hoy el de la bioética", explica el Papa, y añade: "La razón sin

la fe está destinada a perderse en la ilusión de la propia omnipotencia". La cuestión social se convierte en "cuestión antropológica".

La investigación con embriones, la clonación, lamenta el Pontífice, "son promovidas por la cultura actual", que "cree haber

desvelado todo misterio". El Papa teme "una sistemática planificación eugenésica de los nacimientos".

En la Conclusión de la Encíclica, el Papa subraya que

el desarrollo "tiene necesidad de cristianos con los brazos elevados hacia Dios en gesto de oración", de "amor y de perdón,

de renuncia a sí mismos, de acogida al prójimo, de justicia y de paz".

The economy will not

recover until housing prices stabilize. Housing affects not just American families but banks, credit markets and construction

business and jobs. Economics editor David Wessel explains in the video below:

El vicepresidente de Estados Unidos Joe Biden dijo que el gobierno de Barack Obama "subestimó la gravedad

del estado de la economía", pero defendió su paquete de estímulo y consideró que el plan creará más empleos conforme aumenta

su ritmo de gasto.

_________________________________________

Vice President Biden acknowledged today that the administration underestimated the depth of the

economic recession months ago as it prepared a recovery package that is only now beginning to take effect... "The truth

of the matter was, no one anticipated, no one expected that that recovery package would in fact be in a position at this point

of having distributed the bulk of the money."

"DEBT EXPLOSION"

The US economy is lurching towards crisis with long-term interest rates on course

to double, crippling the country’s ability to pay its debts and potentially plunging it into another recession, according

to a study by the US’s own central bank

BECAUSE OF ITS IMPORTANCE AT THIS

CRITICAL TIME, THE FOLLOWING ARTICLE IS FURNISHED IN ITS ENTIRETY:

MOUNTAIN OF DEBT:

Rising debt may be next crisis

by

TOM RAUM

The Founding Fathers left one legacy not celebrated on Independence

Day but which affects us all. It's the national debt.

The country first got into debt to help pay for the Revolutionary

War. Growing ever since, the debt stands today at a staggering $11.4 trillion - equivalent to about $37,000 for each and every

American. And it's expanding by over $1 trillion a year.

The mountain of debt easily could become the next full-fledged

economic crisis without firm action from Washington, economists of all stripes warn.

"Unless we demonstrate a strong commitment to fiscal sustainability

in the longer term, we will have neither financial stability nor healthy economic growth," Federal Reserve Chairman Ben Bernanke

recently told Congress.

Higher taxes, or reduced federal benefits and services - or a

combination of both - may be the inevitable consequences.

The debt is complicating efforts by President Barack Obama and

Congress to cope with the worst recession in decades as stimulus and bailout spending combine with lower tax revenues to widen

the gap.

Interest payments on the debt alone cost $452 billion last year

- the largest federal spending category after Medicare-Medicaid, Social Security and defense. It's quickly crowding out all

other government spending. And the Treasury is finding it harder to find new lenders.

The United States went into the red the first time in 1790 when

it assumed $75 million in the war debts of the Continental Congress.

Alexander Hamilton, the first treasury secretary, said, "A national

debt, if not excessive, will be to us a national blessing."

Some blessing.

Since then, the nation has only been free of debt once, in 1834-1835.

The national debt has expanded during times of war and usually

contracted in times of peace, while staying on a generally upward trajectory. Over the past several decades, it has climbed

sharply - except for a respite from 1998 to 2000, when there were annual budget surpluses, reflecting in large part what turned

out to be an overheated economy.

The debt soared with the wars in Iraq and Afghanistan and economic

stimulus spending under President George W. Bush and now Obama.

The odometer-style "debt clock" near Times Square - put in place

in 1989 when the debt was a mere $2.7 trillion - ran out of numbers and had to be shut down when the debt surged past $10

trillion in 2008.

The clock has since been refurbished so higher numbers fit. There

are several debt clocks on Web sites maintained by public interest groups that let you watch hundreds, thousands, millions

zip by in a matter of seconds.

The debt gap is "something that keeps me awake at night," Obama

says.

He pledged to cut the budget "deficit" roughly in half by the

end of his first term. But "deficit" just means the difference between government receipts and spending in a single budget

year.

This year's deficit is now estimated at about $1.85 trillion.

Deficits don't reflect holdover indebtedness from previous years.

Some spending items - such as emergency appropriations bills and receipts in the Social Security program - aren't included,

either, although they are part of the national debt.

The national debt is a broader, and more telling, way to look

at the government's balance sheets than glancing at deficits.

According to the Treasury Department, which updates the number

"to the penny" every few days, the national debt was $11,518,472,742,288 on Wednesday.

The overall debt is now slightly over 80 percent of the annual

output of the entire U.S. economy, as measured by the gross domestic product.

By historical standards, it's not proportionately as high as during

World War II, when it briefly rose to 120 percent of GDP. But it's still a huge liability.

Also, the United States is not the only nation struggling under

a huge national debt. Among major countries, Japan, Italy, India, France, Germany and Canada have comparable debts as percentages

of their GDPs.

Where does the government borrow all this money from?

The debt is largely financed by the sale of Treasury bonds and

bills. Even today, amid global economic turmoil, those still are seen as one of the world's safest investments.

That's one of the rare upsides of U.S. government borrowing.

Treasury securities are suitable for individual investors and

popular with other countries, especially China, Japan and the Persian Gulf oil exporters, the three top foreign holders of

U.S. debt.

But as the U.S. spends trillions to stabilize the recession-wracked

economy, helping to force down the value of the dollar, the securities become less attractive as investments. Some major foreign

lenders are already paring back on their purchases of U.S. bonds and other securities.

And if major holders of U.S. debt were to flee, it would send

shock waves through the global economy - and sharply force up U.S. interest rates.

As time goes by, demographics suggest things will get worse before

they get better, even after the recession ends, as more baby boomers retire and begin collecting Social Security and Medicare

benefits.

While the president remains personally popular, polls show there

is rising public concern over his handling of the economy and the government's mushrooming debt - and what it might mean for

future generations.

If things can't be turned around, including establishing a more

efficient health care system, "We are on an utterly unsustainable fiscal course," said the White House budget director, Peter

Orszag.

Some budget-restraint activists claim even the debt understates

the nation's true liabilities.

The Peter G. Peterson Foundation, established by a former commerce

secretary and investment banker, argues that the $11.4 trillion debt figures does not take into account roughly $45 trillion

in unlisted liabilities and unfunded retirement and health care commitments.

That would put the nation's full obligations at $56 trillion,

or roughly $184,000 per American, according to this calculation.

at 2009 spring membership meeting of the Institute

of International Finance, June 11, 2009

There isn't much doubt that attempts to enforce strict application of mark-to-market accounting procedures has

contributed to confusion, uncertainty and inconsistencies among financial institutions. There is a strong case for reviewing

the application of so-called “fair value” standards to commercial banks, insurance companies and perhaps certain

other regulated financial institutions.

The problem is not only the difficulty of measuring value in highly disturbed market conditions.

More broadly, strict mark-to-market accounting entirely appropriate for trading operations and investment banks may introduce

a degree of volatility in reporting incompatible with the basic and essential business model of banks which inherently intermediate

maturity and credit risks.

At the same time, we should demand international consistency and professional judgment in setting

accounting standards. Both are today jeopardized. Political bodies in Europe or the United States or any other country are

simply not the appropriate venue for reaching well-considered judgments that can be enforced internationally. Instead, we

need a bit of patience as the International Accounting Standards Board carefully reviews the application of “fair value”

to banks and those other institutions subject to close official scrutiny in reporting.

Extracto de la Conferencia Central de Paul A. Volcker